Creating a cohesive and effective family budget is the cornerstone of achieving long-term financial security and stability. But where do you start? The budgeting process is not simply about restricting spending; it's a strategic roadmap that begins with understanding your current reality and ends with achieving your shared aspirations. This guide walks your family through the essential, step-by-step process of budget creation, from diligently tracking every dollar that moves through your household to leveraging simple rules like the 50/30/20 framework to create a sustainable plan, and ensuring its long-term relevance by adjusting it to meet your family's evolving goals. By embracing these techniques, your family can move beyond financial stress toward collaborative money management and a more secure future.

Tracking Income and Expenses

Tracking income and expenses is the fundamental starting point for effective family budgeting. Families often find themselves managing multiple streams of income and various expenses, which can become overwhelming without a structured approach to money management and financial oversight. By diligently monitoring these financial components, families can gain valuable insights into their spending habits and make informed decisions about their financial future.

To begin tracking income and expenses, families should establish a clear record-keeping system. This can be as simple as a spreadsheet or as advanced as using budgeting software and apps designed for expense tracking. The key is consistency; families should update their records regularly, ideally weekly or monthly, to ensure they capture all financial transactions. This habit enables families to identify spending trends, such as recurring expenses or impulsive purchases, that may need adjustment or elimination.

In addition to tracking individual transactions, families should categorize their expenses into fixed and variable costs. Fixed costs, such as mortgage payments and insurance premiums, are predictable and should be prioritized in the budget. Meanwhile, variable costs, such as groceries and entertainment, can be altered based on the family's financial goals. By understanding these categories, families can allocate their income more effectively and identify areas to cut back to increase savings or pay down debt.

Using technology can significantly enhance the process of tracking income and expenses. Numerous budgeting apps and tools available today allow families to link their bank accounts and credit cards, automatically categorizing transactions for easy review. These tools often provide valuable insights through visual reports and graphs, making it easier to see where money is going and where adjustments can be made. Leveraging budgeting calculators and apps not only saves time but also helps families stay engaged with their financial situation.

Ultimately, tracking income and expenses is about building a better financial future for the family. It empowers families to set realistic financial goals, such as saving for a vacation, building an emergency fund, or planning for retirement. By staying informed about their economic landscape, families can make proactive decisions that align with their values and aspirations. This practice lays the groundwork for adequate financial literacy, ensuring that every family member understands the importance of managing money wisely.

Setting Financial Goals

Setting and incorporating financial goals into a family budget is essential. A budget acts as a tool to allocate resources effectively and ensure that spending aligns with your goals. By identifying specific, measurable, achievable, relevant, and time-bound (SMART) goals, families can create a roadmap that guides their financial decisions. Whether your goal is to save for a family vacation, pay off debt, or build an emergency fund, having clear objectives helps prioritize spending and saving. This structured approach instills discipline and motivates staying on track.

Once you have tracked your income and expenses and have a clear picture of your finances, it’s time to set those SMART goals. A family might decide to save $5,000 for a family vacation within the following year. Breaking this down into monthly savings targets makes it more manageable. Setting a timeline not only provides motivation but also enables families to track their progress. Celebrate milestones along the way to maintain enthusiasm and commitment to your financial objectives.

Creating a Family Budget

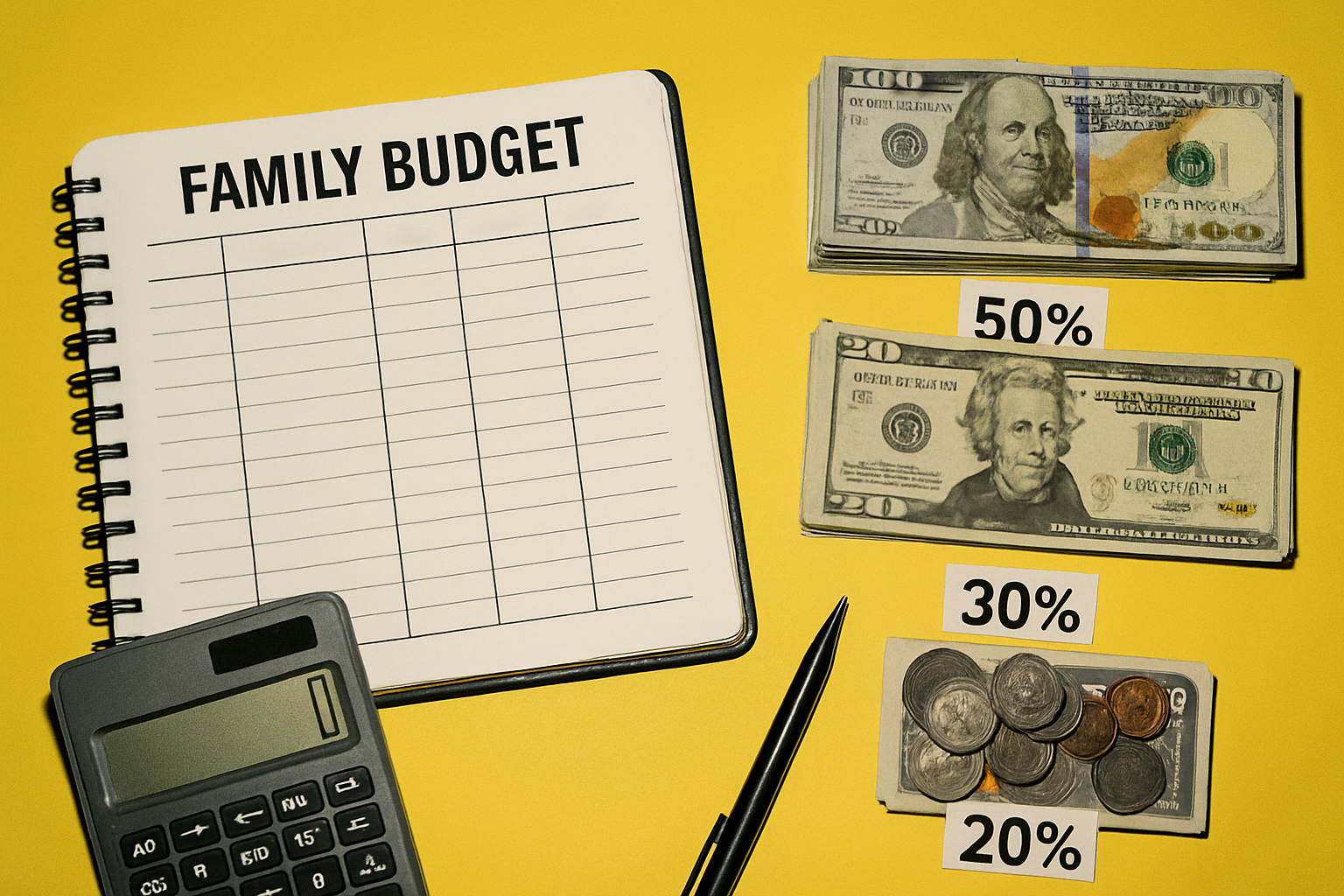

After tracking income and expenses, and setting SMART goals, families can draft a budget that aligns with their goals. The 50/30/20 rule is a simple yet effective budgeting strategy that divides your after-tax income into three distinct categories. This practical method ensures families can manage their finances efficiently while preparing for the future.

- 50% for Needs: This allocation covers all essential expenses and necessary living costs, such as housing, utilities, groceries, health insurance, and transportation. Clearly defining these essential costs is crucial to prioritizing spending and maintaining financial stability.

- 30% for Wants: This portion is reserved for non-essential items and discretionary spending, including dining out, entertainment, travel, and hobbies. Keeping this category in check is key to enjoying life without losing sight of financial goals.

- 20% for Savings and Debt Repayment: The final 20% is vital for financial security, dedicated to building an emergency fund, saving for future goals, or paying down existing high-interest debts. Families should aim for an emergency fund covering three to six months of living expenses.

This framework can serve as a guideline, but families should adjust the percentages based on their unique circumstances. Regularly revisiting and revising the budget ensures it remains relevant as financial situations change, such as new job opportunities or unexpected expenses.

In addition to creating a budget, families should prioritize building an emergency fund. This fund serves as a safety net in the event of unforeseen circumstances, such as medical emergencies or job loss. Ideally, families should aim to save three to six months' worth of expenses in this fund. Starting small and gradually increasing contributions can make this goal more achievable. Having an emergency fund not only provides financial security but also peace of mind, enabling families to make more informed financial decisions without the stress of immediate financial crises.

Involving All Family Members

Involving all family members in the budgeting process is essential in fostering responsibility and teamwork. This collaborative approach helps instill financial literacy from a young age and allows families to set shared financial goals. Discussing finances openly will enable families to address concerns and reinforce positive behaviors.

One effective way to involve everyone is to hold regular family meetings focused on finances. These gatherings encourage accountability and help children understand how financial decisions affect the entire family. Additionally, assigning specific financial responsibilities to each member promotes a sense of ownership. For instance, older children can practice money management skills by tracking expenses or managing a small allowance.

Open communication about money is essential; families should discuss their financial situation candidly to create a supportive environment. Ultimately, this unified approach to budgeting strengthens family bonds and lays the groundwork for lifelong financial literacy.

Adjusting the Budget as Needs Change

Budgeting is not a set-it-and-forget-it process; it requires ongoing adjustments as your family's needs evolve. Life events such as a new job, a child starting college, or medical expenses can significantly impact your financial situation.

One effective method for maintaining alignment is to conduct a weekly or monthly review. During these reviews, identify changes in your spending habits and reallocate funds if necessary. Next, it’s essential to anticipate future expenses, such as vacations or home repair, by forecasting them. Building a sinking fund for these planned expenses minimizes financial strain. Finally, account for fluctuations in income and utilize budgeting tools to streamline the process. This proactive approach helps prevent overspending and ensures your budget remains a sustainable financial plan.

Maintaining Financial Control

Mastering the family budget is an ongoing journey, not a destination. By meticulously tracking your income and expenses, clearly setting SMART financial goals, and consistently applying a framework like the 50/30/20 Rule, your family gains actual control over its economic destiny. The core of this success is communication and teamwork; involving all family members and regularly adjusting your plan ensures that your budget remains a living document aligned with your evolving needs. This commitment to consistent effort and open dialogue will not only safeguard your family against financial uncertainties but will also build a foundation of lifelong financial literacy and prosperity. Start tracking today and take the first step toward achieving your budgeting bliss.